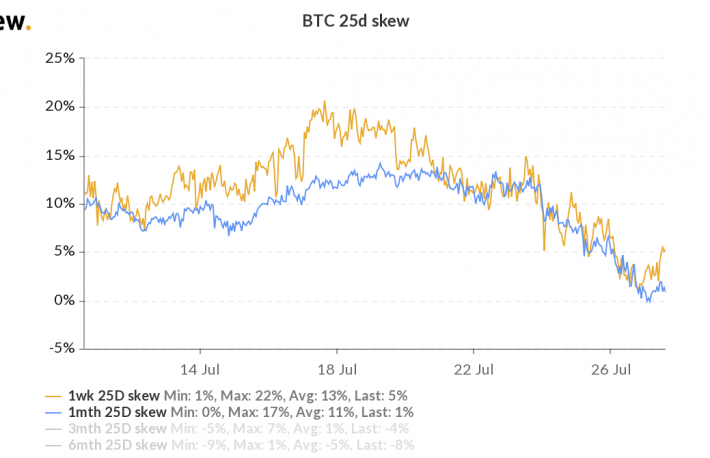

Bitcoin’s one-month put-call skew, which measures the cost of puts, or bearish bets, relative to calls, or bullish bets, has come off sharply to 2% from 13% late last week, according to data provided by crypto derivatives analytics firm Skew. The one-week put-call skew has declined from 13% to 5%.

The narrowing of the spread between prices for puts and calls essentially means investors are no longer seeking downside hedges in anticipation of an extended price drop.

Ether’s one-week and one-month skews have seen similar drawdowns to 0% and 1%, respectively.

The short-term skews have pulled back due to a flurry of call buying. On Friday, a trader bought a total of 2,000 call option contracts on bitcoin in multiple clips of 100 via over-the-counter (OTC) desk Paradigm. The buying was concentrated in July 30 expiry calls at strike prices of $33,000, $34,000 and $35,000. The trader also snapped up Aug. 6 expiry calls at strikes $34,000, $35,000, and $36,000.

Similarly, ether call options saw increased demand over the weekend, as tweeted by Swiss-based data tracking platform Laevitas and Paradigm.

A call option gives the purchaser the right but not the obligation to buy the underlying asset at a predetermined price on or before a specific date. A call buyer is implicitly bullish on the market. A put option gives the right to sell.

While short-dated bitcoin and ether put-call skews have nearly turned neutral from bearish, the longer duration skews remain entrenched in the negative territory, signaling a bullish bias.

At press time, bitcoin is changing hands near $38,500, and ether is trading near $2,300, according to CoinDesk 20 data.

Also read: The Tether Put: Crypto Equivalent of Credit Default Swap?