As usual, the crypto market focused on the immediate narrative: If Elon Musk says that bitcoin (BTC, -9.59%) is bad for the environment, other large investors will probably worry about public scrutiny and decide to sell, right? The expectations game, which consists of guessing what others think you’re thinking, then makes reducing positions the sensible thing to do, regardless of fundamentals.

While this may be Elon Musk speaking before thinking, or it may be his board and/or executives bowing to outside pressure, it’s worth taking a step back to look at the probable motivation and strategy behind the move, as well as its hopeful outcome.

First, let’s look at why the Tesla statement was not that significant, and then we’ll look at why it does actually have meaning.

Against the wind

Tesla announced that it would start accepting bitcoin as payment back in February, at the same time as it announced a $1.5 billion investment in the asset. Even back then, the payment option felt like a PR stunt. If bitcoin is a “reserve asset,” a hedge against fiat debasement, then why would users want to use it as a payment token?

Many insist that bitcoin is useless as a payment token, given its high fees and slow confirmation times. This overlooks the fact that in many areas of the world, it is still a better option than existing systems. And bitcoin-based payment rails are spreading.

However, for the majority of Tesla’s target audience, bitcoin is unlikely to ever be a better payment option than straightforward bank transfers or platinum credit cards. And Tesla’s signaling that bitcoin is a good reserve asset and a useful payment method presents an intellectual disconnect – if bitcoin is worth holding as a fiat debasement hedge, why would users part with it? Especially when, if they needed to raise funds for a Tesla and had lots of bitcoin sitting idle, they could use the cryptocurrency as collateral for a fiat loan, which could then go toward a shiny new car.

In other words, the number of Tesla customers excited about paying with bitcoin was always going to be small to nonexistent.

Removing that option feels like another PR stunt, and a ham-fisted one at that. The economic impact of removing something hardly anyone would want anyway is negligible, both for Tesla and for the demand for bitcoin.

The reason given for the decision was “the rapidly increasing use of fossil fuels for Bitcoin mining and transactions.” This is factually false. More detailed information on this is not hard to find. And Tesla confirmed that it is not selling its current stake in BTC.

So, with this move, Tesla comes across as one, lazy and irresponsible on the research side – Tesla shareholders have every right to wonder why the company is just finding out about the energy consumption mix now – and two, hypocritical: Why is supposedly contaminating BTC acceptable for the balance sheet, but not as a possible (but unlikely) convenience to users?

As for credibility, when Twitter co-founder Jack Dorsey tweeted last month that “Bitcoin incentivizes green energy,” Elon Musk responded: “True.”

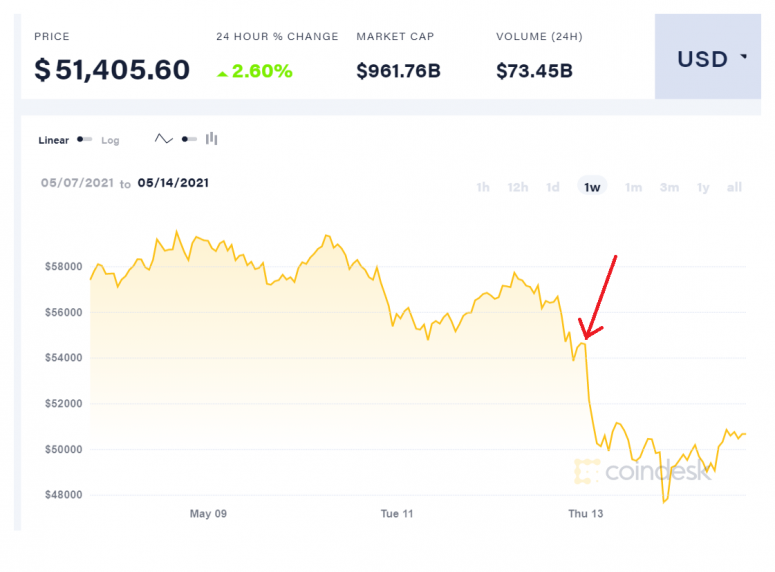

And, you have a potential breach of fiduciary duty, something Elon Musk is no stranger to. With this tweet, the price of BTC dropped almost 8% within three hours, producing a significant slump in the market value of the firm’s bitcoin holdings. (This will not impact the balance sheet, which values bitcoin at the lower of cost or market value.)

Elon Musk may act irresponsibly at times, which is a risk that Tesla shareholders know about and accept. But he is far from stupid. So what is really going on here?

A place in the sun

I am not a mind reader and have no insider knowledge of the thought process behind publishing that statement. But I don’t think it was an impetuous mistake.

Tesla’s mission, according to the headline on the “About” section of its website, is to “accelerate the world’s transition to sustainable energy.” Last week, Tesla entered the S&P 500 ESG Index (up 9.8% year to date at time of writing, slightly ahead of the S&P 500), which selects stocks based on environmental, social and corporate governance scores relative to others in the same industry group. And earlier this week, with uncanny timing, Reuters reported that Tesla was seeking entry into the multibillion-dollar U.S. renewable fuel credit market.

So Tesla has invested heavily in sustainable energy and it has invested heavily in bitcoin. Might we soon see Tesla-branded “green” bitcoin mining?

With the bitcoin payments statement, Musk is kicking the bitcoin-is-bad-for-the-environment conversation up a notch. The flood of counterarguments his tweet received is just the beginning. But with Musk’s tweet and the subsequent price fall, the community is no doubt becoming even more acutely aware that tweeting is not enough. Writing reports is not enough. This conversation needs to escalate to policy.

A rising tide

What does that mean? It could range from fiscal incentives to spend more on energy R&D to outright operational bans unless the energy mix meets certain criteria. There’s also the tool of energy subsidy tweaks.

Incentives are generally good – bans not so much – but the objective would be to nudge mining firms along the energy transformation curve. Many have been doing this anyway.

And officials are waking up to the potential to attract cryptocurrency-related businesses to their areas. In many cases, bitcoin mining can boost activity in struggling economies that have good natural resources but low infrastructure spend.

Tough times lie ahead for officials and regulators when it comes to harnessing the opportunity in crypto. Many of them are still relatively low on the learning curve. We all know that environmental questions are complicated, the problems are often misunderstood and “simple” fixes are anything but. Throw into the mix the still controversial concept of decentralized self-sovereign currencies, and you have the considerable challenge of identifying social priorities, let alone protecting them.

But the more bitcoin mining gets talked about at a policy level, the more “acceptable” it becomes as an industrial activity. Politicians will come to realize that bans will merely send the activity elsewhere. The more the potential is understood, the greater the incentive for politicians to come up with solutions that help remove the contamination stigma. And the greater the mining industry involvement in renewable energy initiatives, the cleaner its image will become, removing a potentially significant barrier to more widespread investment in the bitcoin market.

That’s how the Tesla decision ends up helping the bitcoin price: by escalating a much-needed conversation that will end up removing investment barriers and encouraging further development and exploration of the role bitcoin can play in many fundamental areas of society.

Stablecoin shifts

This week saw what could be the start of a meaningful shift in the stablecoin market.

The largest stablecoin by far is tether (USDT, -0.14%) (USDT), which has for years been grappling with a cloud of suspicion that its tokens are not fully backed by dollar reserves. This week, we found out that those suspicions were correct.

Part of the recent settlement with the New York Attorney General’s office stipulated that Tether would publish quarterly breakdowns of its reserves. It did so this week, in the form of pie charts with no mention of an independent review by an accounting firm.

The pie charts showed that almost half of all reserves (65% of the 75% “cash & cash equivalents”) is held in commercial paper, which is not always liquid, nor does it reliably hold its value. Understandably, this has made many market participants nervous, although tether’s continued growth even through worse uncertainty indicates that, for most, its liquidity and ubiquity are more important. Tether has a much more significant role as a trading pair and a much higher outstanding supply than other cryptocurrencies.

That might be about to change. Earlier this week, crypto exchange FTX – one of the top five crypto derivatives exchanges in terms of volume, according to skew.com – and its retail subsidiary Blockfolio started allowing users to fund their accounts with the second-largest stablecoin, USDC (-0.11%).

And Diem, formerly Facebook-linked Libra, is partnering with Silvergate Bank to launch a U.S. dollar-pegged stablecoin. This is a far cry from the global ambitions of the original project, which aimed to put the convenience of blockchain-based electronic money in the wallets of all Facebook users – the network will be permissioned, accessible only to approved participants, so the extent of its reach remains to be seen. It is significant, however, in that it is the first time we have a U.S. bank launching a stablecoin.

Tether will likely continue to dominate the stablecoin market for some time, despite weakening confidence in its backing (which was never very strong anyway). But numbers are also pointing to a shift: In the second half of 2020 and so far in 2021, supply growth in the other top four stablecoins in terms of market capitalization has easily outpaced that of the market leader.

Chain Links

Swiss financial giant UBS Group is in the early stages of planning to offer digital currency investments to affluent clients, according to a Bloomberg report. TAKEAWAY: Last week it was Citi, the week before that it was U.S. Bank. In March, it was Goldman Sachs and Morgan Stanley. In February, it was BNY Mellon and Deutsche Bank. The growing roster of high-profile legacy names getting involved in crypto markets in various ways is raising expectations for the second half of 2021. If we think these financial institutions are big, we should remember that they got there on the back of big clients.

Investment bank Cowen Inc. will offer crypto custody services to hedge funds and asset managers. TAKEAWAY: Cowen may not be as well known as names such as UBS, but it is over 100 years old and represents a profound shift in institutional attitudes toward this “rebel” market.

U.S. hedge fund giants Millennium Management, Point72 Asset Management and Matrix Capital Management are all at varying stages of launching cryptocurrency-focused trading funds, with plans to start earning returns using decentralized finance (DeFi) platforms, according to sources. TAKEAWAY: DeFi used to be something that institutions feared, didn’t trust, wanted to ignore. Not any longer. We’ve seen accelerating signs that interest in DeFi functionality and investment is growing. This is astonishing, given that most DeFi platforms have not been audited, have no oversight and have relatively low liquidity (by institutional standards). It is also exciting in that more money entering the ecosystem brings attention, funding, legitimacy and more scrutiny.

Crypto asset manager Bitwise has launched a new ETF, the Bitwise Crypto Industry Innovators ETF (NYSE:BITQ), which offers investors exposure to companies that derive at least 75% of their revenue from or have 75% of their net assets in cryptocurrencies. TAKEAWAY: This offers a convenient exposure to the industry, with the additional variable of corporate strategy. Going forward, as more crypto companies go public, corporate strategy will become a more significant selection factor, allowing investors to complement direct investment in crypto assets with the potential upside (or downside) of business risk. Until then, given the lack of listed crypto vehicles in the U.S., funds like these are likely to act as a proxy for the overall crypto market.

Renaissance Technologies seems to be following a similar strategy. This week it disclosed multi-million dollar positions at the end of Q1 2021 in several listed crypto mining stocks: Riot Blockchain ($61.8 million), Marathon ($75 million) and Canaan ($4.2 million). TAKEAWAY: These positions are tiny relative to the fund’s $115 billion in AUM, but meaningful compared to the companies’ size – they account for approximately 3% of Riot’s and Marathon’s market cap. What is notable is that these positions were all accumulated during the first quarter. This implies that Renaissance could switch out of them at any time, which could trigger significant volatility in the respective share prices.