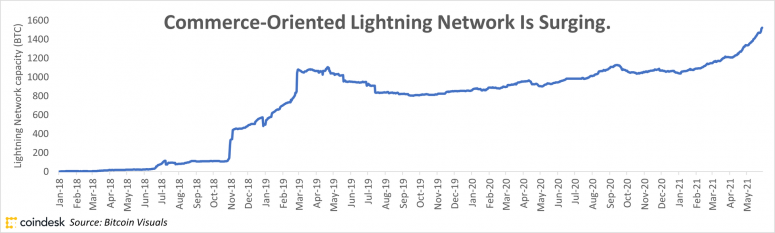

The best bellwether for bitcoin’s use in commerce is the Lightning Network. Briefly, Lightning is a commerce-friendly service that sits on top of Bitcoin. It allows parties to transact quickly and cheaply, verifying their transactions periodically in batches via the more trust-minimized Bitcoin network.

As we noted in last week’s Chain Links, Lightning has been surging this year. As of this Tuesday, the number of bitcoin available for use on its network had increased by 44% since Dec. 31.

That’s something for bitcoin’s potential use in commerce. But we’d be remiss not to consider it next to Bitcoin’s use on another network that is more associated with finance than with commerce – Ethereum.

Wrapped Bitcoin (WBTC (-3.62%)) is an Ethereum-compliant (ERC-20) token that is pegged to the value of bitcoin. The peg is maintained by the custodian BitGo.

The number of bitcoin wrapped on Ethereum has grown faster (67%) over the same period, and it’s a couple orders of magnitude greater than the number of bitcoin committed to the Lightning Network: As of this Tuesday, the supply of WBTC was 188,961. Lightning Network’s bitcoin capacity was 1,523.

In theory, it’s possible that WBTC could be used on commercial applications that accept ERC-20 tokens. In reality, it’s used for decentralized finance (DeFi).

The story of these two charts is clear, at least for now: bitcoin is much more like gold, an investment, than it is like the dollar, a medium of exchange.

Michael Saylor went on CoinDesk TV this week and talked about that distinction, describing a world in which citizens of dollarized, bitcoin-adopting countries like El Salvador have digital wallets holding multiple cryptocurrencies: One currency is a stablecoin pegged to the dollar; the other is bitcoin, an investment.

That’s where Saylor departed the text. “It’ll move on Bitcoin rails,” he said, talking about that dollar stablecoin, leading to further dollarization across the world. The possibility of dollarization via stablecoins is real, but as for what rails it will move on, the market has spoken: It’s not Bitcoin, it’s Ethereum.

The chart above shows the supply of tether (USDT, -0.08%) (USDT), the largest stablecoin by supply, on three networks that support it. The nearly flat line is tether on Omni, an application-supporting layer that runs on Bitcoin, and tether’s original network. The line that goes up and to the right-hand corner of the chart is tether on Ethereum.

Tether and other stablecoins certainly have the potential to facilitate commerce, better than more volatile cryptocurrencies, which are more suited to investment. However, in reality their use is in finance, specifically as a quote currency on cryptocurrency exchanges.

In sum, it’s finance, not commerce, that is leading adoption of crypto, and while bitcoin enjoys a unique status as the blue-chip investment in this category, the market is showing a clear preference for rails built on Ethereum.

That brings to mind another bit of thought leadership that went out over crypto’s digital TV airwaves this week: Steve Hanke, a Johns Hopkins economist, said El Salvador’s new bitcoin policy will make it a hub for criminals looking to launder bitcoin into dollars. (My bitcoin maximalist friends will quickly point out that Amsterdam and Frankfurt have recently served as quite convenient money-laundering hubs.)

As the above chart shows, there is no shortage of demand for dollar-pegged stablecoins. The crypto exchanges offering liquid bitcoin-tether crosses are many, and some of them, I suspect, do not have the most stringent KYC/AML. Crypto-to-dollar pairs are fewer, and if a world like Saylor describes truly comes to pass, the regulatory challenges at the ramps between crypto and commerce will extend far beyond the borders of one Central American nation-state.